|

MONETARY POLICY Monetary policy is a type of demand management, stabilization policy.

|

Chapter 14, Money and Banking, is a relatively short and easy chapter so I have little to add in this online lecture.

As was mentioned last week, unit 3 is on Macroeconomic POLICIES. Chapter 10 and 12 covered FISCAL POLICY - using government spending and taxes to stabilize the economy. the next three chapters 14, 15, and 16, cover MONETARY POLICY. You may want to review the online lecture on macroeconomic policy (see http://www.harpercollege.edu/mhealy/eco212i/lectures/ch13-18.htm#pol) . Here I will just quickly review the monetary policy section:

MONETARY POLICY

Monetary policy is a type of demand management, stabilization policy.There are two types of monetary policy

- easy money policy or expansionary monetary policy

- tight money policy or contractionary monetary policy

The goal of an easy policy is to reduce unemployment. Therefore the tool would be an increase in the money supply. This would shift the AD curve to the right decreasing unemployment, but it may also cause some inflation.

MS

¯ Interest Rates

The goal of a tight money policy is to reduce inflation. Therefore the tool would be a decrease in the money supply. This would shift the AD curve to the left decreasing inflation, but it may also cause some unemployment.

MS

As we studied in chapter 12 (aggregate demand/aggregate supply) and chapter 10/13 (fiscal policy), there are two types of demand management policy (1) fiscal policy and (2) monetary policy). They both shift the aggregate demand curve in order to reduce unemployment or inflation. The main difference between fiscal and monetary policy is WHO conducts the policy. Fiscal policy is undertaken by the US Congress and the US President. The congress may pass a new law to reduce taxes in order to increase aggregate demand and fight unemployment and the president signs it. The congress and the president ultimately need to report to the voters.

Who conducts monetary policy and to whom do they report

Monetary policy is conducted by the Federal Reserve, commonly called the "Fed". To be more precise, monetary policy is conducted by a committee of the Fed called the Federal Open Market Committee (FOMC). We will learn in this chapter that the Fed is NOT the federal government and that the FOMC is made up of only 12 people. Some are appointed by the US president, but others are not.

We will begin our study of monetary policy in this chapter with two important topics: (1) what is money?, and (2) what is the "Fed"?

Learning objectives - In this chapter students will learn:

1. The functions of money and the components of the U.S. money supply.

2. What "backs" the money supply, making us willing to accept it as payment.

3. The makeup of the Federal Reserve and the U.S. banking system.

4. The functions and responsibilities of the Federal Reserve.

1. Circular Flow Model of CapitalismWhich of the arrows in the figure below represent money flow? Flows (1) and (4) represent money. Flow (1) represents costs and income money flows and flow (4) represents consumer expenditures and business receipts money flows.

2. Money facilitates trade, promotes specialization, and therefore reduces scarcity

Without money there would be barter. Barter is the direct exchange of goods and services for other goods and services. We discussed the problem with barter in the lesson on trade.We learned that without money there would be less trade and therefore less specialization and more productive inefficiency. Therefore, from the same quantity of resources, LESS would be produced. This is because money avoids the "double coincidence of wants" and allows for more specialization and productive efficiency. The "double coincidence of wants" is a situation in which the good or services that one trader desires to obtain is the same as that which another desires to give up and an item that the second trader wishes to acquire is the same as that which the first trader desires to surrender. In other words, you have to find somebody who wants to trade the item that you want to get AND who also wants the item that you have that you want to trade. Therefore, money allows us to use our limited resources wisely and produce MORE with the same amount of resources. This helps to reduce scarcity, because if you can't find someone to trade with, you will have to produce it yourself.

3. Money and the Aggregate Demand / Aggregate Supply Model

In chapter 12 we said that the money supply is a determinant of AD because of its effects on interest rates and investment.If: MS

If: MS

Almost anything can be, and has been, used as money. the textbook says "money is what money does" - or anything that does what money does, IS money. People have used cattle, cigarettes, shells, stones, gold, and even beer as money. So what does money do?Functions of Money

Money has three important functions. It is a:1. Medium of exchange: Money can be used for buying and selling goods and services. We buy things with money this enables us to avoid the double coincidence of wants of barter and therefore reduce scarcity.2. Unit of account: Prices are quoted in dollars and cents. We can use monetary values to compare apples and oranges

3. Store of value: Money allows us to transfer purchasing power from present to future. I can work today , earn some wealth, and save that wealth as money so that I can spend it later. I could also save my wealth as gold, or shares of stocks. What make money different is that it is the most liquid (spendable) of all assets and therefore a convenient way to store wealth.

|

REVIEW:

|

Components of the Money Supply

So, what is the "Money Supply" (MS)?

REVIEW - In chapter 12 we said that:If: MS

If: MSThe textbook discusses the two different measures of the money supply:

1. M1

2. M2

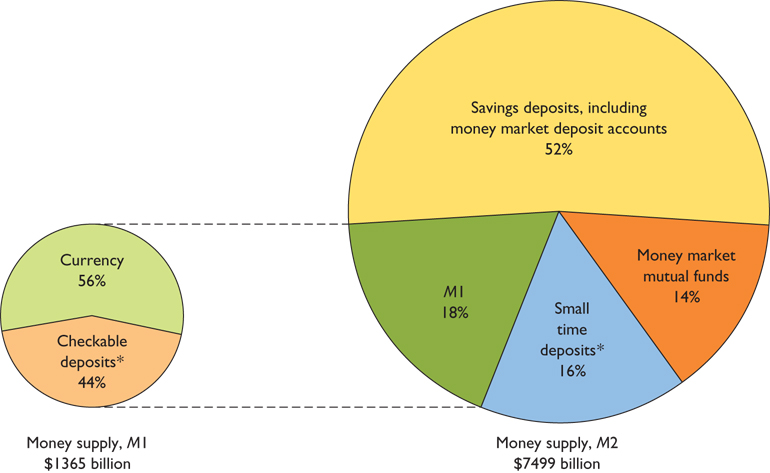

1. M1a. the most liquid definition of the money supply: they are directly and immediately usable as a medium of exchangeb. M1 includes:

- currency (coins and paper money) held by the public (what WE have in our purses, wallets, and homes)

- checkable deposit (NOTE: nearly half of the M1 money supply is what WE have in our checking accounts.

c. Review: If I take $10 from my wallet and put it into my checking account, what happens to M1?

If I take $10 from my wallet and put it into my checking account, what happens to M1?

M1 does not change d. The following are NOT part of M1:

- currency in banks

- currency and checkable deposits owned by the government

- currency and checkable deposits owned by the Federal Reserve Banks

2. Money Definition: M2

a. M2 is a little less liquid than M1b. M2 includes:

- M1

- Savings deposits and money market deposit accounts.

- Certificates of deposit (time accounts) less than $100,000.

- Money market mutual fund balances, which can be redeemed by phone calls, checks, or through the Internet.

- Review: If I take $10 out of my wallet and put it into my savings account

- what happens to M1?

- what happens to M2?

If I take $10 out of my wallet and put it into my savings account

- what happens to M1?

- It decreases by $10

- what happens to M2?

- It does not change, Remember, M2 includes M1

Which definitions are used? M1 is simplest and often cited, but M2 is often used by economists. The text will ignore the distinctions and focus on the more general concept of the money supply, keeping in mind that changes in M1 components will also change M2.

Consider This … Are Credit Cards Money?

Credit cards are not money, but their use involves short term loans; their convenience allows you to keep M1 balances low because you need less for daily purchases.

Graph - If we were to graph the money supply (either M1 or M2, ) it would look like the graph below WHICH WE WILL USE IN CHAPTER 16 TO SHOW HOW MONETARY POLICY WORKS. This graph shows the money supply to be $400 billion, but if we are using the real M1 we can see from the figure above it should be $1364 billion.

When we say:

MSWhich measure of the MS should we use?

- we will use M1 just to keep it simple

- economists generally use M2

- M2 is important because it can easily be changed into M1 types of money and influence people's spending of income.

- The ease of shifting between M1 and M2 complicates the task of controlling the spendable money supply.

What is not money?

1. currency and checkable deposits of the government, Federal Reserve, and banks

2. income is not money

- income is a FLOW concept: you earn income over time (e.g. $500 a week)

- money is a STOCK concept: you have a given amount at a point in time ( e.g. $500 in your wallet and checking account right now)

- when we talk about "money demand" we will mean a demand for more liquidity (more in my wallet) NOT an increase in my income

- Can you get an increase in your income and have less money?

- YES, if you put more of your income in the stock market and less in your checking account

3. credit cards

- Credit cards are not money, but their use involves short-term loans; their convenience allows you to keep M1 balances low because you need less for daily purchases.

Why is money "money"? -- What "backs" the money supply?

A. The government's ability to keep its value stable provides the backing.B. Money is debt; paper money is a debt of Federal Reserve Banks and checkable deposits are liabilities of banks and thrifts because depositors own them.

C. Value of money arises not from its intrinsic value, but its value in exchange for goods and services.

1. It is acceptable as a medium of exchange.2. Currency is legal tender or fiat money. In general, it must be accepted in repayment of debt, but that doesn't mean that private firms and government are mandated to accept cash; alternative means of payment may be required. (Note that checks are not legal tender but, in fact, are generally acceptable in exchange for goods, services, and resources. Legal cases have essentially determined that pennies are not legal tender.)

3. The relative scarcity of money compared to goods and services will allow money to retain its purchasing power.

D. Money's purchasing power determines its value. Higher prices mean less purchasing power. (Key Question #6)

E. Excessive inflation may make money worthless and unacceptable. An extreme example of this was German hyperinflation after World War I, which made the mark worth less than 1 billionth of its former value within a four-year period.

1. Worthless money leads to use of other currencies that are more stable.2. Worthless money may lead to barter exchange system.

F. Maintaining the value of money

1. The government tries to keep supply stable with appropriate fiscal policy.2. Monetary policy tries to keep money relatively scarce to maintain its purchasing power, while expanding enough to allow the economy to grow.

Money DemandWhat is it?

- MD is our demand for liquidity

- it is our demand to keep some of our wealth in our wallets, purses, and checking accounts

- it is NOT a request for higher wages at work

The Demand for Money: Two Components

There are two sources of money demand or two reasons why do we want to hold M1 money in our wallets, purses, and in our checking account, instead of putting it in the back to earn interest. They are the (1) transactions demand and the (2) asset demand. The (3) Total demand for money (keeping money in our wallets and not in our savings account where they can earn interest) then is the transactions demand plus the asset demand.Transactions Demand for Money

Definition:

- We keep M1 money in order to buy things

- It is the demand for money as a medium of exchange

Transactions demand and nominal GDP

- directly related: when GDP increases the transactions demand for money also increases (shifts to the right).

- the main determinant of transactions demand is nominal GDP

Transactions demand and interest rates

- we'll assume that they are unrelated, so on a graph the transactions demand looks like:

Graphically

Asset demand

Definition:

- we keep some money so that we can spend it later

- the demand for money as a store of value

What determines how much money (M1) we keep in our wallets, purses, and checking accounts?

- The problem with holding money: is that you are not earning interest on it

- Asset demand and interest rates are inversely related

- if interest rates are high, people will keep less in their pockets and more in their savings accounts (and in other interest earning assets)

- if interest rates are low, people will keep more money in their pockets, because they are not losing much and it is more convenient

Therefore, graphically, the asset demand for money looks like:

According to this graph, if interest rates on savings accounts are 10%, the quantity of money that we STORE in our wallets and checking accounts will be zero. Note: we would still keep some to buy things (transactions demand).

According to this graph, if interest rates on savings accounts are 10%, the quantity of money that we STORE in our wallets and checking accounts will be zero. Note: we would still keep some to buy things (transactions demand).Total Money Demand

- Total MD = transactions demand + asset demand

- Graphically: The black vertical D1 is the transactions demand and the black, downward sloping D2 is the asset demand. If we add them together we get the blue total demand for money.

The Market for Money: Interaction of Money Supply and Demand

Now lets add the MS (money supply) graph from above. The graph below and textbook's Key Graph 16.1c illustrates the money market. It combines demand with supply of money.If the quantity demanded exceeds the quantity supplied, people sell assets like bonds to get money. This causes bond supply to rise, bond prices to fall, and a higher market rate of interest.

If the quantity supplied exceeds the quantity demanded, people reduce money holdings by buying other assets like bonds. Bond prices rise, and lower market rates of interest result (see example in text).

The Money Market

Graph:

The Federal Reserve and the Banking System

See:Know:

- Board of governors

- Federal Open Market Committee (FOMC)

- 12 Federal Reserve Banks

The Federal Reserve System (the "Fed") was established by Congress in 1913 and holds power over the money and banking system.

1. The figure below gives framework of Fed and its relationship to the public.

2. The central controlling authority for the system is the Board of Governors and has seven members appointed by the President for staggered 14 year terms. Its power means the system operates like a central bank.

Board of Governors

- seven members

- appointed by the US president and confirmed by the senate

- 14 year terms

- the US president selects the chairperson (currently Ben Bernanke)

3. The Federal Open Market Committee (FOMC) includes the seven governors plus five regional Federal Reserve Bank presidents whose terms alternate. They set policy on buying and selling of government bonds, the most important type of monetary policy, and meet several times each year.

FOMC

- 12 members:

- the 7 members of the BOG

- the president of the New York Federal Reserve Bank

- 4 of the other 12 Fed bank presidents on a rotating basis

- conduct open market operations (Open Market Operations [OMO] - see chapter 14)

4. The system has twelve districts, each with its own district bank and two or three branch banks. They help implement Fed policy and are advisory.

- they act like a central bank coordinated by the Fed BOG

- quasi-public banks

- each Federal Reserve Bank is owned by the private commercial banks in its district

- but the BOG, a government body, sets the basic policies

- making a profit is not their goal, any profits go to the U.S. Treasury.

- goal is to help the economy

- a bank for banks

- banks keep deposits at the Fed. these are the the RESERVES of the banks.

- banks take out loans from the Fed (the Discount Rate [DR)] see chapter 14). In making loans, the Federal Reserve is the "lender of last resort," meaning that the Fed is available to lend money should other avenues (e.g. other commercial banks) not be available.

5. There are about 7,300 commercial banks in the United States. They are privately owned and consist of state banks (three-fourths of total) and large national banks (chartered by the Federal government).

6. Thrift institutions consist of savings and loan associations, credit unions, and mutual savings banks. They are regulated by the Treasury Dept. Office of Thrift Supervision, but they may use services of the Fed and keep reserves on deposit at the Fed. Of the approximately 11,000 thrift institutions, most are credit unions.

Functions of the Fed and money supply:

1. The Fed issues "Federal Reserve Notes," the paper currency used in the U.S. monetary system.

2. The Fed sets reserve requirements and holds the reserves of banks and thrifts not held as vault cash.

3. The Fed may lend money to banks and thrifts, charging them an interest rate called the discount rate.

4. The Fed provides a check collection service for banks (checks are also cleared locally or by private clearing firms).

5. Federal Reserve System acts as the fiscal agent for the Federal government.

6. The Federal Reserve System supervises member banks.

7. Monetary policy and control of the money supply is the "major function" of the Fed.In chapter 14 we will learn that the Fed has 3 TOOLS for controlling the money supply (and hence control unemployment and inflation). these 3 tool are:

1. OMO (open market operations - function #7 above)

2. Discount Rate (DR function # 4 above)

3. RR (Reserve Requirement - function #2 above)

Federal Reserve independence is important but is also controversial from time to time. Advocates of independence fear that more political ties would cause the Fed to follow expansionary policies and create too much inflation, leading to an unstable currency such as that in other countries

The Federal reserve is quite independent of political control

- The BOG is appointed by the president, BUT

- for 14 year terms

Controversy

- Advocates of independence fear that more political ties would cause the Fed to follow expansionary policies and create too much inflation, leading to an unstable currency such as exists in some other countries

- Most countries maintain political control over their central banks

- The 12 members of the FOMC can decide to decrease the MS (to fight inflation) and put millions of people out of work and there is little recourse. Politicians may complain but they can do little.

SUMMARY

---------

Recent Developments in Money and Banking

A. Relative decline of banks and thrifts: Several other types of firms offer financial services.B. Consolidation among banks and thrifts: Because of failures and mergers, there are fewer banks and thrifts today. Since 1990, there has been a decline of 5200 banks.

C. Convergence of services provided has made financial institutions more similar: See text on new laws of 1996 and 1999 that made many changes possible.

D. Globalization of financial markets: Significant integration of world financial markets is occurring and recent advances in computer and communications technology suggest the trend is likely to accelerate.

E. Electronic payments: Internet buying and selling (including PayPal), Fedwire transfers, and "smart cards" are examples. In the future, nearly all payments could be made with a personal computer or "smart card."

LAST WORD: The Global Greenback

A. An estimated $450 billion of U.S. currency is circulating abroad.1. $450 billion is about 60% of the total U.S. currency held by the public.2. Russians hold about $80 billion because dollar value is stable, however recently some Russians have transferred their holdings to euros.

3. Argentina holds $50 billion and fixes its own peso exchange rate to dollar reserves.

B. U.S. profits when dollars stay overseas: It costs us 4¢ to print each dollar and to get the dollar; foreigners must sell Americans $1 worth of products. Americans gain 96¢ over cost of printing the dollar. It's like someone buying a traveler's check and never cashing it.

C. Black markets and illegal activity overseas also are usually conducted in dollars because they are such a stable form of currency.

D. Overall, the "global greenback" is a positive economic force. It is a reliable medium of exchange, measure, and store of value that facilitates transactions everywhere and there is little danger that all the dollars will return to U.S.